Business Times – 24 Apr 2008

NEWS ANALYSIS

Same figures in flash estimate of property prices can be read very differently

By ARTHUR SIM

THE property price index (PPI) for the first quarter of 2008 will be released soon – and is unlikely to differ from an earlier flash estimate of a 4 per cent increase, despite developers starting to cut prices for new projects.

So how useful is the PPI? Does data overload cause confusion?

Last week, The Straits Times headline for the story on the flash estimate was ‘Private homes sales recover in weak market’. In The Business Times, the headline was ‘Private home sales tumble, prices weaken’.

As confusing as it sounds, both headlines were technically correct.

One reason could be how data is interpreted and the level of optimism or pessimism – the same figures can be read very differently.

Consider the flash PPI for Q1, which increased despite the quarter being one of the worst in recent years for new sales. Yet the consensus appeared to be that the PPI could still rise this year.

The PPI is essentially a transaction-based index. Properties are split into segments to form sub-indices that are then used to calculate the PPI.

The Urban Redevelopment Authority (URA) uses the moving-average method to compute the weights assigned to the various sub-indices. The weights, updated quarterly, are based on the moving average mix of transactions over the past 12 quarters.

While the PPI is widely used as the gauge of Singapore’s property market, this method is not used universally.

In the United States, for instance, analysts are more likely to refer to ‘housing starts’ – the number of homes being built – as a gauge of the market, or more importantly, market sentiment.

There are also indices based on the prices of resale homes alone, as some believe this is a more accurate measure of prices the market will bear.

In Singapore, Jones Lang LaSalle (JLL) has been looking at other ways to track and gauge property price movements.

Recently, JLL’s head of research (South-east Asia) Chua Yang Liang started to monitor the lowest-transacted median prices of properties in the Outside Core Region because he believes these are a more accurate reflection of price tolerance.

While such an index is in the works, Dr Chua says there could also be variables, pertaining to property size and location, that could have a significant bearing.

Recognising that the property market is becoming more fragmented, with the high-end sector in particular supported by foreigners and speculators, URA has provided separate PPIs for different regions, with the Outside Central Region being one and the Core Central Region and Rest of Central Region the other two.

But this has itself led to speculation on which region is performing better.

In one of its more pro-active moves, URA also began releasing monthly data on developer sales in the middle of last year when the market was most ‘exuberant’.

While the rationale at the time was to make pricing of new launches even more transparent, it has inadvertently revealed how prices can be skewed.

Part of this could be due to developers sometimes selling units selectively to ensure prices remain high.

An optimist will interpret this as prices remaining stable, while a pessimist will only see that demand has fallen.

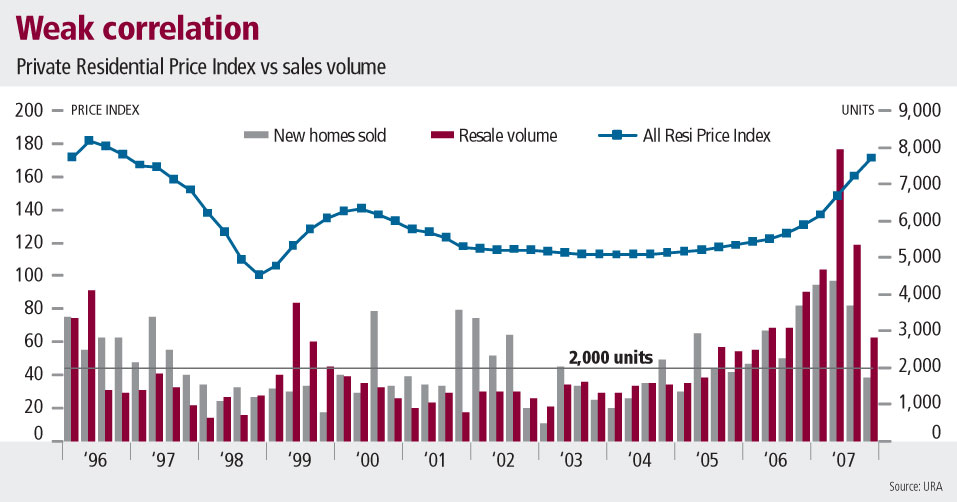

For the current PPI to be meaningful, there should be some correlation with sales volume, as both are tied to the basic mechanics of supply and demand.

However, after comparing sales volume against the PPI since the previous peak in the mid-1990s, no strong correlation could be determined.

One contrarian trend did emerge, and this was that since the last trough in Q4 1998, the PPI is more likely to rise as transaction volumes fall. Unfortunately, this only adds to the confusion.